Cost of goods sold definition

The cost of goods sold is the sum of all costs directly associated with the production of goods. It covers the costs of raw materials and labor and appears on the income statement. The cost of marketing, sales, and distribution is excluded from COGS.

Is your manufacturing business really profitable? The correct answer lies in one important accounting term – Cost of Goods Sold.

Evaluating COGS clearly justifies your business’s profitability. It includes all direct costs incurred in the production or purchasing of goods. Labor costs and raw materials are direct expense examples. However, indirect costs, such as sales, marketing, and distribution, are not included here.

Knowing how to calculate COGS is very important for all businesses of any size. From pricing strategies to tax reporting, it plays a crucial role.

📌 Key takeaways

- Cost of goods sold includes all the direct expenses incurred in the production.

- Accurate COGS helps business professionals to accurately determine profitability.

- Professionals can improve overall financial performance by lowering COGS.

- To determine COGS, sum all direct costs associated with producing the goods or services sold.

- COGS management can be improved by accurately tracking inventory and using accounting software.

What is the cost of goods sold (COGS)?

Cost of goods sold refers to the total cost the company incurred in producing or purchasing the product. Direct labor expenses, cost of raw material, and shipping charges are such costs.

This cost varies with production, which is why it is sometimes known as a variable cost. In contrast, indirect costs such as office rent, utilities, and insurance are constant. These are commonly known as fixed expenses.

Manufacturing units primarily use COGS. The agriculture, telecommunications, food, and construction sectors are such industries where it play a crucial role. Service-based companies use the cost-of-service term rather than COGS. However, the purpose of both terms is the same.

Why COGS matters in the business world?

COGS is a valuable term in the business world. By understanding it, you can easily measure the business’s profitability. Also, it allows you to determine gross profit by subtracting direct production costs from revenue.

Business professionals reduce their taxable income because COGS is a deductible expense. The cost of goods sold also enables professionals to optimize their pricing strategy. This contributes to upholding a satisfactory margin for sustainable income.

It also supports better inventory management. Business professionals can easily understand the cost of inventory sold. Thus, it gives a clear scenario of how much inventory is sold and left. This helps maintain and manage stock levels and inventory planning.

Investors and other financial experts also rely on COGS. They can easily determine the company’s financial condition by evaluating it.

What does COGS include?

As mentioned earlier, COGS covers all costs directly associated with manufacturing or purchasing the product. The major components of cost of goods sold are as follows:

- Raw material costs – The cost of necessary materials incurred for the production of the product.

- Direct labor costs – The salary and wages paid to the laborers involved in the production.

- Manufacturing overhead – Indirect production expenses, such as machine maintenance and safety tools, that support manufacturing.

- Inventory costs – The total cost incurred in maintaining inventory.

- Packaging costs – The expenditure on boxing, labeling, and packaging of the product.

- Shipping and freight costs – The transportation charges applied during the shipping of the product.

- Production supply costs – The total expenditure on buying the supporting materials for the production.

What is excluded from COGS?

Indirect operating costs are usually excluded from COGS. These are commonly known as Selling, General and Administrative (SG&A). The common expenses not included in COGS are as follows:

- Office rent and utilities – This is a recurring expense for office lease and utility bills.

- Accounting and legal fees – The payment that you pay to the accountant and legal advisor.

- Marketing – The expenditure for the business publicity and promotion.

- Employee salary (not related to production) – The salary you pay to your staff who are not directly involved in the production.

- Taxation – Business taxes that you pay, as these are not directly related to manufacturing.

- Customer support and administrative costs – Expenses related to office administration and customer service.

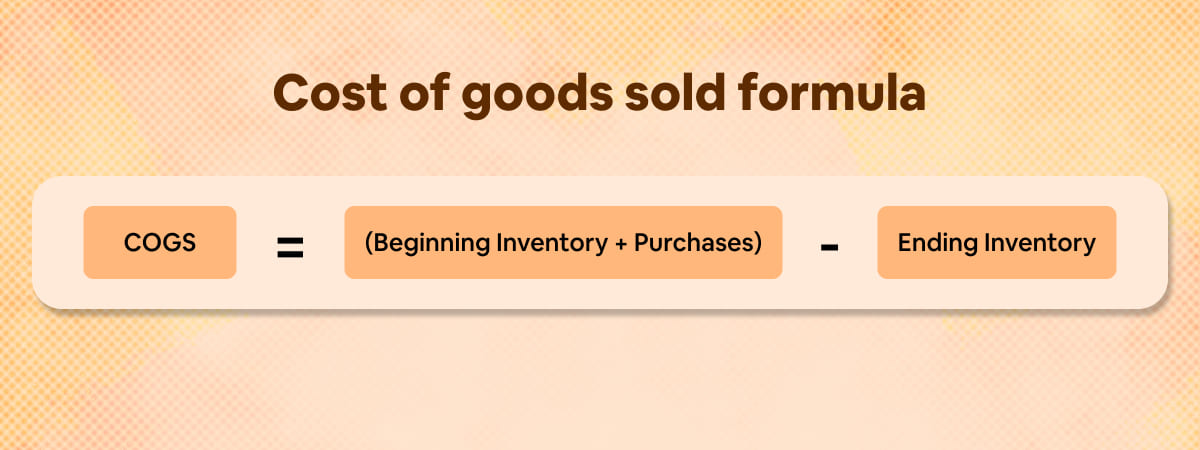

What is the Cost of Goods Sold formula?

What is COGS? Till now, we’ve found the answer and understood it well. Further, you must also know how to find it. However, before that, you must be aware of the cost of goods sold formula, which is as follows:

Here,

- Beginning inventory – Inventory value at the beginning of the accounting period.

- Purchases – Additional inventory or production costs incurred during the period.

- Ending inventory – Unsold inventory remaining at the end of the period.

How is the cost of goods sold calculated?

After understanding what cost of goods sold is and its formula, let’s look at how to calculate COGS. Here are the four steps of calculation:

1. Identify direct costs

Initially, you need to identify all costs associated with the product’s production and purchase. It covers the direct labor, raw materials, and packaging costs.

2. Finding the beginning inventory

Determine the inventory value at the initial period.

3. Calculate the purchase during the period

Sum up all the inventory purchases made during the period. This helps determine the total number of items available for sale.

4. Calculating ending inventory

Now, find out the unsold inventory value at the end of the period.

Once you determine the beginning inventory value, purchase cost, and ending inventory value, you can directly use them in the COGS formula.

Cost of goods sold example

Let’s understand it with the COGS example. Suppose a business professional sold 10 chairs, each priced at $1,000, at the start of the year. Later in the same month, he purchased 4 chairs from the vendor, but sold only 1 out of them, along with the 10 chairs. At the end of the year, the inventory value of unsold chairs is counted as $3,000.

- Beginning inventory = 10 chairs worth $10,000

- Purchased inventory = 4 chairs worth $4,000

- Total chairs sold = 11 chairs worth $11,000

- Ending inventory = $3,000 (3 unsold chairs)

Then, according to the formula –

($11,000 + $4,000) – $3,000 = $12,000

So, the company’s COGS is $12,000

Still stuck with the manual financial management?

Simplify financial reporting and stay business-ready with accurate and clean reports.

What are the different accounting methods?

There are four accounting methods: FIFO, LIFO, average cost, and specific identification. Let’s understand them one by one:

1. FIFO

Under this method, the oldest inventory items are sold first. It means the newest inventory remains in the stock. This method tends to lower COGS when prices are high. So, companies using FIFO often gain higher net income.

2. LIFO

According to LIFO, the newest produced or purchased products are sold first. This leads to higher COGS and lower net income when professionals sell during the height of the price period.

3. Average cost method

In this method, the average cost per unit is applied to all sold items and to the remaining inventory. It means individual purchase costs are not tracked separately; instead, a weighted average cost is used for valuation.

4. Specific identification method

In this method, each inventory item is tracked individually based on its cost. This method is very useful for customized and high-value products. When the item is sold, the cost is assigned directly to the COGS.

How does inventory affect COGS?

Inventory directly affects the cost of goods sold by determining cost allocation between sold goods and remaining stock. Several methods, such as FIFO and LIFO, are used to determine COGS. Whether the inventory level increases or decreases, it directly affects the COGS value in such ways:

- Higher ending inventory = Low COGS value

- Lower ending inventory = High COGS value

- Increased inventory purchases = Higher inventory available for sale, which affects COGS based on the sales volume.

The COGS value decreases when the ending inventory is higher because fewer items are sold. Likewise, the COGS value increases when inventory levels are low because more goods are sold.

In short, purchases increase inventory levels. However, COGS depends on how many items are sold from inventory.

How does Moon Invoice help in managing COGS?

Reputable invoicing software, such as Moon Invoice, does not automatically calculate COGS. However, it helps manage expenses, inventory, and financial reporting more efficiently through its advanced digital features.

You can efficiently manage all business costs in a centralized system with no manual effort. The system allows recording and categorizing expenses such as raw materials, labor, shipping, and manufacturing. This categorization makes your business cost tracking more efficient.

The system supports 15+ custom business reports. You can easily get financial insights in real time with little effort. You can instantly generate profit-and-loss statements, inventory reports, and expense summaries. These accurate insights help professionals understand the cost structure and calculate COGS accurately.

Moon Invoice reduces manual errors and improves control over cost-related information. Ultimately, you can make better decisions with the correct information.

Control business expenses without the spreadsheet struggle

Digitalize your expense management with Moon Invoice to improve your business’s financial operations.

Ending words

Understanding and calculating the cost of goods sold is essential for maintaining profitability and making informed decisions. You can also set the right pricing strategies and overall financial performance with accurate COGS. Additionally, choosing the right accounting software can further enhance your management. Ultimately, you can strengthen your financial operations.

Common questions on COGS

What is the cost of goods sold formula?

How do you find your COGS?

What are the main components of COGS?

Are salaries covered in COGS?

Is COGS identical to the production cost?

We at Moon Invoice, are the best minds behind smarter invoicing and seamless business growth. We love to solve financial problems and keep providing effective tips through our blogs, newsletters, and social media channels. As a team, we continue exchanging ideas about growing financial challenges and smart use of automation tools.