![What is Payment Reconciliation? [Types, Examples & Best Practices]](https://mi-blogs.s3.amazonaws.com/mi-live/blog/wp-content/uploads/2026/02/26071955/Payment-Reconciliation-960x560.jpg)

Payment reconciliation definition

It is a common accounting practice to match the transaction data with the internal payment records in order to maintain accuracy.

Modern businesses thrive on an ecosystem of payments, vendors, and invoicing. Of these, payments move much faster through multiple gateways such as user renews their subscriptions, or when someone from your team processes the refund. Everything looks perfect until the numbers stop matching, and that’s really scary.

Discrepancy in transaction or a duplicate entry of the same payment can quickly throw your books off balance, leading to time-consuming investigations later. This further underscores why finance professionals label payment reconciliation as one of the most detail-intensive and cumbersome tasks.

Our business finance guide breaks down what is payment reconciliation, the payment reconciliation process, and best practices. Right then, let’s first start with the online payment reconciliation.

What is Payment Reconciliation?

Payment reconciliation refers to the practice where the accounting team compares the business transactions with the internal records (usually the company’s general ledger). It aims to maintain your books clean and transparent by verifying payment records against invoices or purchase orders.

Simply put, reconciliation of payments aids businesses in ensuring the received money is actually what is recorded in the entries. This way, reconcile payments not only tell a true story of the cash flow but also offer glitch-free reporting.

How Does Payment Reconciliation Work?

Following the reconciliation payment meaning, let us demonstrate how the payment reconciliation process usually works.

1. Accumulate Data

The payment reconciliation process begins with the collection of required documents. Before you dig through transactions, it’s necessary to have all bank statements, invoices, transaction details, and other necessary documents in hand. In addition to that, you will need sales receipts, purchase orders, as well as data from journal entries. If the documents are recorded digitally in your personal device, keep them ready to initiate the scrutiny process.

2. Cross-check Transactions

After collecting the data, the accounting team starts vetting payment transactions against each invoice or purchase order. They verify the amount paid or received by comparing it with the corresponding incoming or outgoing invoices. For instance, they match the paid amount with the vendor invoice by referring to the said amount and verifying the bank statement.

3. Make Adjustments

While verifying the payment transaction, if any discrepancies are found, the accounting team examines the matter in detail and makes the necessary adjustments to the records. Here, discrepancies could be the result of fraudulent activities or honest human mistakes.

Either way, the records must be corrected in a way that ensures accuracy in the accounting books. However, in case there are no discrepancies throughout the verification process, the team can directly proceed with the final review process.

4. Review & Finalize

In the last step, the account manager or any authorized person is responsible for reviewing the updated records. They take a closer look at reconciliation statements to verify that discrepancies have been properly resolved. Plus, they view related invoices, payment receipts, or bank statements before giving final approval. And that’s how the payment reconciliation keeps everything accurate and well-documented.

Nobody Enjoys Hunting Down Missing Payments

Nor do they enjoy fixing messy books at month-end. Automate reconciliation with Moon Invoice and avoid spending hours chasing transactions.

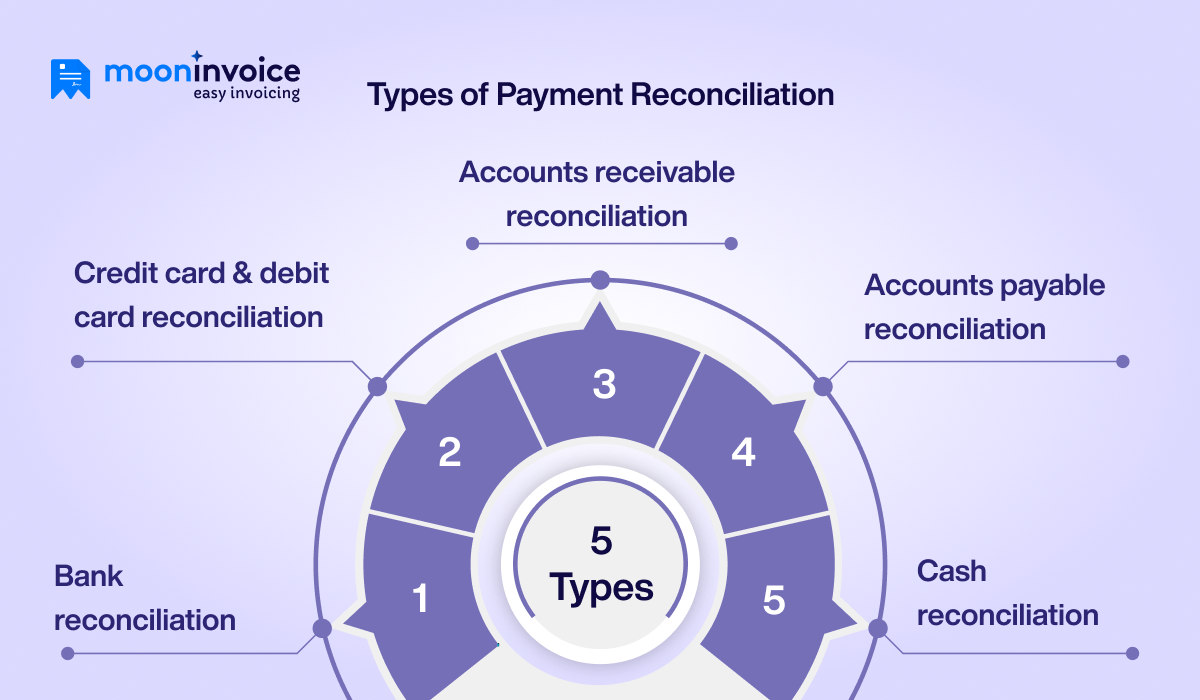

Various Types of Payment Reconciliation

Here are a few payment reconciliation types to consider while ensuring accuracy in your financial reports.

1. Bank reconciliation

As the name suggests, it’s another accounting practice to match the completed transactions with the bank statements. It aims to keep the reports accurate by maintaining a balance between cash deposits and the bank reports.

2. Credit card and Debit card reconciliation

Akin to the bank reconciliation, credit and debit reconciliation only considers transactions made through credit and debit cards. The process involves comparing the monthly statements with the internal company records in a bid to spot unauthorized transactions.

3. Accounts receivable reconciliation

Reconciling accounts receivable is another type, where accountants compare customer payments with already issued invoices. Such practice is mainly followed to resolve underpayment or overpayment issues.

4. Accounts payable reconciliation

In the AP reconciliation process, the accounting team concentrates on matching supplier or vendor invoices with the amount they need to pay. AP reconciliation aids accountants in knowing whether they are paying what they actually owe.

5. Cash reconciliation

Reconciling cash refers to double-checking what the business has already recorded in the books. With this approach, the accountant counts the available cash in order to match the numbers recorded in the books.

Why Businesses Must Reconcile Payments? – Importance Explained

If you are running a business, then reconciliation of payments is as important as cash flow management. Here are a few more reasons why every business must follow the reconciliation process.

1. Early error detections

While reconciling the payment, one can flag minor errors or mismatches in the early stages. Preventing them early means avoiding a snowball effect, where small issues escalate into larger financial problems.

2. Less disputes

Since the reconciliation process is making sure every document gets verified, chances are too less for customer disputes. Reviewing the documents leaves no chance of underpayment or overpayment, which reduces the chances of disagreements.

3. Better compliance

Payment reconciliation, when done frequently, helps you comply with tax rules and regulations. It ensures the recorded figures equate to the successfully completed transactions, which further keeps reports audit-ready and lowers the risk of penalties.

4. Accuracy in reporting

Reconciliation of payments makes sure that income, expenses, and balances are correctly recorded in the reports, giving business owners a crystal clear view of financial performance. After all, financial reports are only as reliable as the data behind them.

5. Cash and debt management

Daily performing the reconciliation process also aids in clear visibility into where your money moves. A clarity that further allows you to plan business finances more effectively and manage the company’s short-term debt obligations.

Best Practices for Payment Reconciliation

Here are the top accounting practices to follow while reconciling the payments for better accuracy.

- Make reconciliation a part of your routine activity to identify discrepancies as early as possible.

- Assign one person to handle financial transactions and another to review and reconcile.

- Utilize smart tools or software to automate the reconciliation process, so that your team can speed up the work.

- Always keep proper documentation after making adjustments, and if possible, attach notes so that records are clear for future audits.

- Try to address the discrepancies in less time to prevent larger financial issues in the near future.

- Ask an experienced person to thoroughly review the reports, which adds one extra layer of accuracy.

- When discrepancies pop up, collaborate with vendors and payment providers to obtain the required information.

What are the Challenges in Payment Reconciliation?

Here are some risks associated with payment reconciliation, especially if done manually.

- Missing or incomplete records: Manual payment reconciliation carries a high risk of missing proper data, which leads to incomplete financial records. The problem doesn’t end there because it will also impact the tax filing process.

- No real-time sync: Business can’t sync the payment data in real time because there is no option to integrate the accounting books. Every time you need to copy-paste the data utilizing conventional bookkeeping practices to update the details.

- Reporting errors: Small reporting errors are unavoidable with a manual payment reconciliation approach. A challenge that is usually caused by repetitive entries and can make the financial statements inaccurate.

- Payment complexity: Another serious issue when reconciling payments manually because successful transactions do not always match in one format. The real trouble arises when you have transactions made in multiple currencies.

- Compliance risk: When reconciliation of payments is highly error-prone, it carries a compliance risk and doubles the chances of discrepancies. What then follows is tax miscalculations and weak audit trails.

Reconcile Your Payments With Moon Invoice – Effortlessly

We understand how painful it is to manually reconcile the payment transactions. That’s why we built Moon Invoice differently to cater to your reconciliation needs. Moon Invoice is not just another traditional software, but a powerful tool that does the heavy lifting for you.

Moon Invoice lets you reconcile the transactions smoothly and accurately – no lengthy paperwork or manual calculations. The software reconciles transactions on your command and gives you a clear view of payments made against each invoice.

That’s how it guarantees the transactions recorded in this payment reconciliation system are in accordance with what you have actually earned. As a result, you don’t have to worry about accuracy and data security as well. All you can have is accurate financial reports and better visibility into the cash flow.

Try Stress-free Reconciliation with Moon Invoice

Let Moon Invoice help you keep records squeaky clean.

Real-time updates

Bank reconciliation

Accurate reports

Final Thoughts on Payment Reconciliation

Reconciliation of payment is all about creating an accurate financial records and keeping payment data well organized. By doing so, businesses can get rid of discrepancies in the early stages and prepare audit-ready reports to forecast finances.

This accounting practice focus on maintaining accurate and transparent payment information. Utilizing online payment reconciliation system, businesses can take a benefit of real-time sync and keep the payment data up to date. This means no need of spending hours on manually comparing the details or extra paperwork.

A few clicks and you get a magnified view of completed payment against issued invoices. Want to try by yourself? Start your free trial now.

General Queries Answered

Can payment reconciliation be automated?

How does payment reconciliation help cash flow?

What is the difference between payment reconciliation and bank reconciliation?

We at Moon Invoice, are the best minds behind smarter invoicing and seamless business growth. We love to solve financial problems and keep providing effective tips through our blogs, newsletters, and social media channels. As a team, we continue exchanging ideas about growing financial challenges and smart use of automation tools.