Profit and loss statement definition:

A profit and loss statement is a financial report that summarizes a business’s revenue, expenses, profits, and losses over a specific period to evaluate overall financial performance and profitability.

A profit and loss statement is one of the most important financial reports that showcases how your business is performing. It includes revenue, expenses, and profit over a specific period, which lets you know whether your business is growing over time or losing money.

For accountants and finance teams, the P&L statement is even more essential as it helps spot trends, identify spending patterns, and plan the budget for the next financial year. Apart from that, P&L statements also play a massive role in ensuring compliance with tax regulations.

So, how should you prepare your P&L statement? This is where many professionals lack clarity in preparing accurate financial reports.

In this blog, we will understand in detail what a profit and loss statement is, along with its types, examples, and how you should prepare one. Let’s get started…

📌 Key Takeaways

- P&L statements help you determine the profitability or losses incurred by the business in a specific period.

- There are four common types of P&L statements, namely single-step, mult-step, condensed, and common-sized.

- To prepare the profit and loss statement for your business, first calculate the total revenue.

- Incorrect expense categorization and overlooking manual calculation errors are among the top P&L mistakes to avoid for accountants.

- You should consider using accounting software to make quick, error-free P&L statements.

What is a profit and loss statement?

A profit and loss statement, popularly known as a P&L statement or income statement, is an important financial report of a business that includes revenues, expenses, and profits over a specific period. By reviewing P&L statements, businesses understand whether they are growing or facing losses.

Businesses generally prepare quarterly, half-yearly, or annual P&L statements to track their financial performance and make cost-effective decisions for the future. Business owners, accountants, and other finance authorities review a business’s P&L statement to assess its profitability and overall financial health.

Struggling to generate accurate P&L statements?

Utilize Moon Invoice, where you can view automated and error-free P&L summaries in seconds. Make smart business decisions with zero manual hassle.

Types of profit and loss statements

There are multiple types of profit & loss statements, and each one works differently. Based on your business size and reporting needs, you need to choose the appropriate type of profit and loss statement.

Below are the most common types of profit and loss statements:

1. Single-step profit & loss statement

If you are searching for a profit and loss statement for small business, this could be your answer. A single-step P&L statement is the simplest type of P&L statement. Here, the net profit is calculated by subtracting total expenses from the total revenue. In single-step P&L statements, the entire calculation is done once and is hence called a single-step profit loss statement.

Small businesses, startups, and sole proprietors mostly use this profit & loss statement because it is easy to prepare and understand.

2. Multi-step profit & loss statement

A multi-step P&L statement is a more detailed version of the normal profit and loss statement. Unlike single-step, here the calculation doesn’t complete in one step. In multi-step, the operating revenue and expenses are separated from non-operating items to have more clarity on the business’s actual profitability.

Mostly medium and large-scale businesses use this format to track profit margins and analyze operational efficiency in a better way.

3. Condensed profit & loss statement

A condensed P&L statement can also be called a hybrid of multi-step and single-step statements. It showcases the most important financial items and groups similar financial items together. It doesn’t include every single transaction or expense except the important ones.

Many businesses use condensed profit loss statements for investor presentations, quick financial reviews, and internal management reporting.

4. Common-sized profit & loss statement

A common-sized P&L statement is another type of profit and loss statement in which each line item is expressed as a percentage of total revenue rather than shown as absolute amounts. As a result, businesses can compare their financial performance across different periods rather than a single period. Businesses can also compare their financial performance against competitors regardless of company size.

Common-sized P&L statements are generally used for financial analysis, identifying cost trends, and comparing business performance over time.

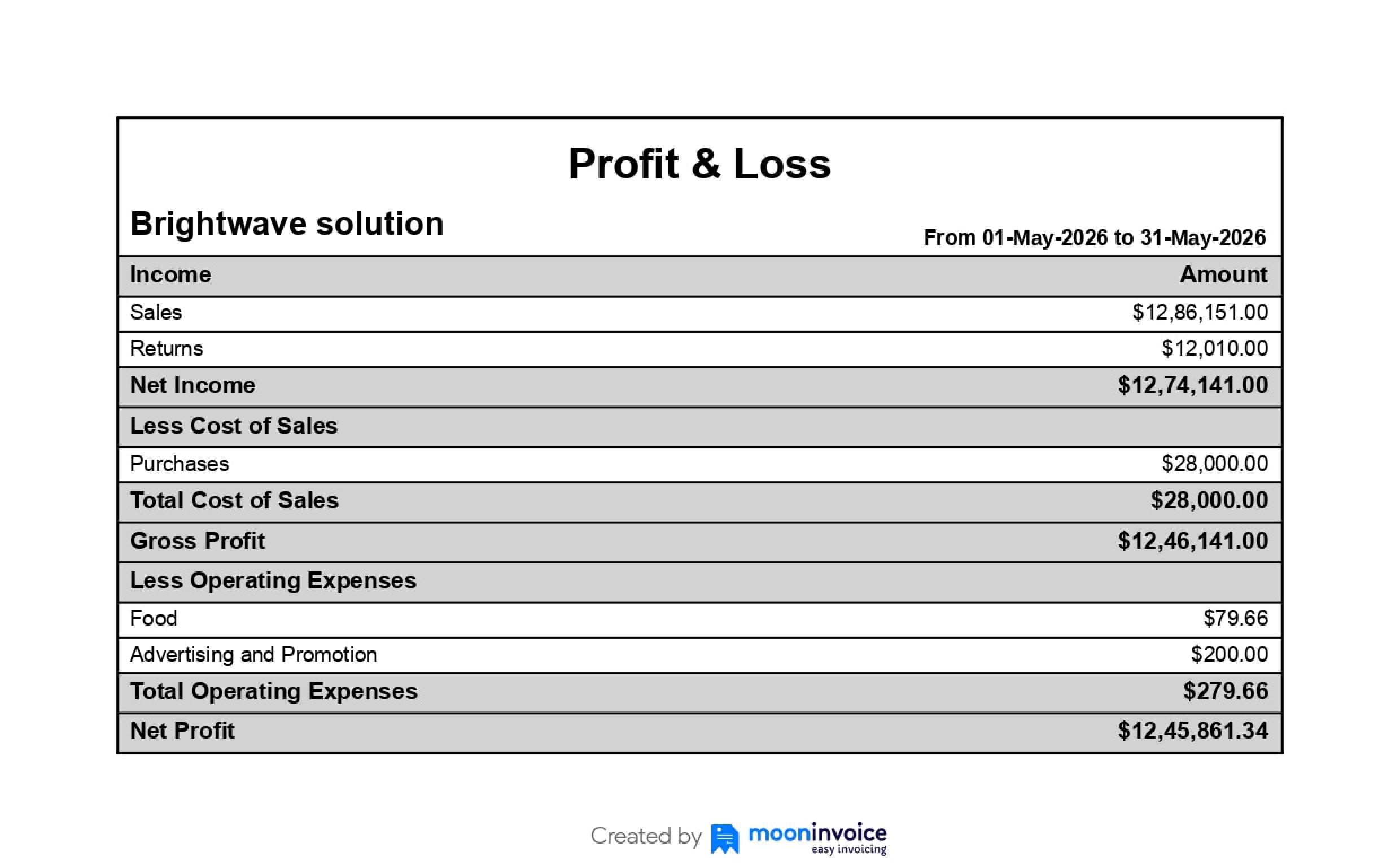

Profit and loss statement example

The following is a P&L statement example used in businesses:

How do profit and loss statements work?

To understand how a profit and loss statement works, we first need to determine what type of P&L it is. For example, a simple P&L statement provides a basic summary of financial data for an overview of profits and losses. But, a more detailed P&L statement may include total sales and expenses data, gross profit, COGS, and other related terms.

Also, it is key to note that some P&L statements showcase comparative financials from previous periods, such as year-over-year, so the accounting team can compare changes in profits and losses over time.

Here’s how they work:

1. Revenue

Revenue is generally called the “top line” as it appears at the top of the profit & loss statement. It serves as the starting point for all calculations.

Revenue includes the total income earned from business operations, such as product sales, services, subscriptions, and other primary activities. To prepare a P&L statement for your business, firstly, you need to find out the total revenue, for which you can use the following formula:

2. Cost of Goods Sold (COGS)

Once revenue is recorded, businesses calculate the cost of goods sold (COGS) for that specific period. COGS is the direct cost of producing goods or delivering services, including direct labor, manufacturing costs, etc. To determine the COGS of your business, you can use the formula:

3. Gross profit

Next, businesses record gross profit, which shows how efficiently they produce and sell their products or services before deducting operational expenses.

A higher gross profit means the company has a stronger profit margin and is producing goods and services more efficiently.

Here’s how you can find the gross profit of your business:

4. Operating expenses

After recording gross profit, businesses look to subtract operating expenses from it. Operating expenses are the daily business expenses that play a major role in running the business.

Operating expenses include:

- Staff salaries

- Rent and utilities

- Marketing expenses

- Office supplies

- Insurance costs

These costs are not directly linked to manufacturing products, but are necessary to keep business operations stable.

5. Operating income

Once operating expenses are deducted, the remaining amount is termed operating income or operating profit. It is the profit generated from core business operations before deducting taxes, interest, or non-operating activities.

The formula to calculate operating income is:

6. Non-operating items

After recording operating income, businesses account for non-operating items. These items are clearly separated from normal business operations but still play a big role in calculating the company’s overall profitability.

Non-operating items include:

- Interest income or expenses

- Investment gains or losses

- Taxes

- One-time expenses

- Asset sale profits

7. Net income or net loss

After calculating everything, lastly comes the net income or net loss. It is the amount that represents the company’s final earnings or losses after deducting expenses, taxes, and additional costs.

The formula to calculate net income (or net loss) is:

If the amount is positive, it is a profit and is termed “net income”. If the amount is negative, it is a loss and is termed a “net loss”.

How to make a profit and loss statement?

Creating a P&L statement manually could be a tedious task, especially for businesses with high transaction volumes. Manual P&L statements could lead to calculation errors and time-consuming processes. On the other hand, if you use accounting software, you can create it in just a few steps.

Here are the steps to create profit and loss statement using accounting software.

Step 1: Choose your accounting software

Do your research and find the best accounting software that fits your needs. Generally, accounting software comes with many other reporting features apart from P&L reports, such as the ability to create quarterly reports, summary reports, and profit by product reports that reduce your accounts team’s workload.

Step 2: Prepare reports with auto-calculation

Once you utilize accounting software in your business workflow, start managing finances with it. The software will record every invoice, expense, estimate, credit note, and debit note your business deals with in an organized manner. Later, you can check your business’s P&L statement by heading to the “reports” section and clicking “profit and loss report”.

Step 3: Review thoroughly

The P&L statement lists sales, returns, net income, purchases, gross profit, operating expenses, non-operating expenses, and net profit. You need to review each item to determine whether your business has made a profit or incurred a loss. Each figure in a P&L statement carries significant value, so you need to review it thoroughly and ensure there are no calculation errors.

How to read a profit and loss statement?

Small business owners or startups are often confused by the many figures on the P&L statement. The correct way to read a profit and loss statement is by reviewing the company’s total revenue first. Next, you should check the cost of goods sold (COGS), operating expenses, and finally the net profit or loss.

By reviewing the P&L statement in this way, you will easily understand profits made by the company, money spent by the company, and whether operations remained profitable for that particular period.

The profit and loss statement helps evaluate the company’s financial health by showing detailed figures of revenue and expenses. When profit & loss statements are analyzed alongside other financial statements, such as balance sheets and cash flow statements, you will gain a clear understanding of operational efficiency and long-term financial stability.

Escape the endless loop of errors and corrections

Transform your manual P&L report creation into an automated financial process.

One-click report generation

Automatic calculation

Real-time insights

Common mistakes to avoid while creating P&L statements

Below are some of the most common mistakes to avoid while creating P&L statements:

- Combining personal and business expenses: Mixing personal purchases with business expenses can affect the profit calculations and cause problems during tax filing.

- Incorrect expense categorization: Not organizing expenses into proper categories can lead to inaccurate reporting and difficulty tracking operational costs.

- Relying entirely on manual calculations: Manually creating P&L statements instead of using accounting software may cause calculation errors and delays in preparing the statement.

- Ignoring non-cash expenses: Not including depreciation and amortization is another mistake to avoid while creating P&L statements. Since it affects your profitability, ignoring non-cash expenses could be costly for you.

How often should you prepare P&L statements?

Ideally, businesses should prepare P&L statements monthly, quarterly, or annually to easily identify financial trends, reduce unnecessary spending, and plan growth strategies.

The reason you should prepare P&L statements regularly is that they indicate the profit or loss your business is making for a specific period. By looking at the statement, you can control expenses and plan your budget for the next financial year.

Auto-generate P&L statements using accounting software

P&L statements are undeniably important for any business. For business owners, it helps them understand their current financial position and acquire funds from investors or lenders. When P&L statements show positive figures, your business has greater potential to grow and expand in the long run. This is the primary reason you should prepare P&L statements carefully, as simple errors can cost you dearly.

When you create P&L statements manually, there is a higher risk of errors and missing data, which can cause delays. On the other hand, with advanced accounting software such as Moon Invoice, you can generate P&L statements automatically. Just one click, and your reports are ready.

Apart from P&L statements, Moon Invoice also helps you create other reports, such as summary reports, quarterly reports, profit by product reports, invoice aging reports, expense reports, and more. The automated process keeps your financial reports organized and gives better visibility into your financial performance.

So, what are you waiting for? Get started with Moon Invoice today!

FAQs on Profit and Loss Statements

How to create profit and loss statement?

What is the P&L formula?

Who needs profit and loss statements?

Can I check the P&L of my own business?

What are the common profit and loss statement mistakes?

We at Moon Invoice, are the best minds behind smarter invoicing and seamless business growth. We love to solve financial problems and keep providing effective tips through our blogs, newsletters, and social media channels. As a team, we continue exchanging ideas about growing financial challenges and smart use of automation tools.