In the high-stakes game of construction and contracting, achieving prosperity goes beyond delivering outstanding results – it’s about safeguarding your interests against life’s curveballs. No matter who you are – a general contractor spearheading colossal ventures, a budding entrepreneur carving a niche in the trades sector, or a homeowner embarking on remodeling escapades – grasping the crux of contractor insurance is non-negotiable.

As market analyses predict, the global construction insurance landscape is set to witness a steady upswing, anticipated to clock a commendable Compound Annual Growth Rate (CAGR) exceeding 4.5% over the forthcoming decade spanning 2021–2030.

This guide will equip you with business insurance policies, commercial auto insurance, workers compensation insurance, business liability insurance, etc.

Let’s dive into the world of contractor insurance, how to have cheap contractor insurance, and pave the way for a secure and successful contracting journey, including general contractor insurance requirements.

What is Contractor Insurance?

Contractor insurance, alternatively referred to as construction insurance or contracting business insurance, represents a tailored variety of coverage explicitly engineered to fortify persons and enterprises engaged in the domain of construction plus contracting.

Acting as a reliable economic safeguard, this insurance offering delivers broad-spectrum defense against numerous threats coupled with accountabilities characteristic to the profession.

Several types of policies are available under contractor insurance depending on one’s specific needs, including general liability insurance policies, tools & equipment insurance; commercial auto policy; umbrella/excess liability coverage, among others. We will discuss general contractor insurance requirements later in the blog.

Obtaining cheap contractor insurance depends largely upon factors such as the size & scope of projects being handled alongside assessment based on potential risks involved during the execution stage, thus ensuring safety standards compliance throughout the project lifecycle.

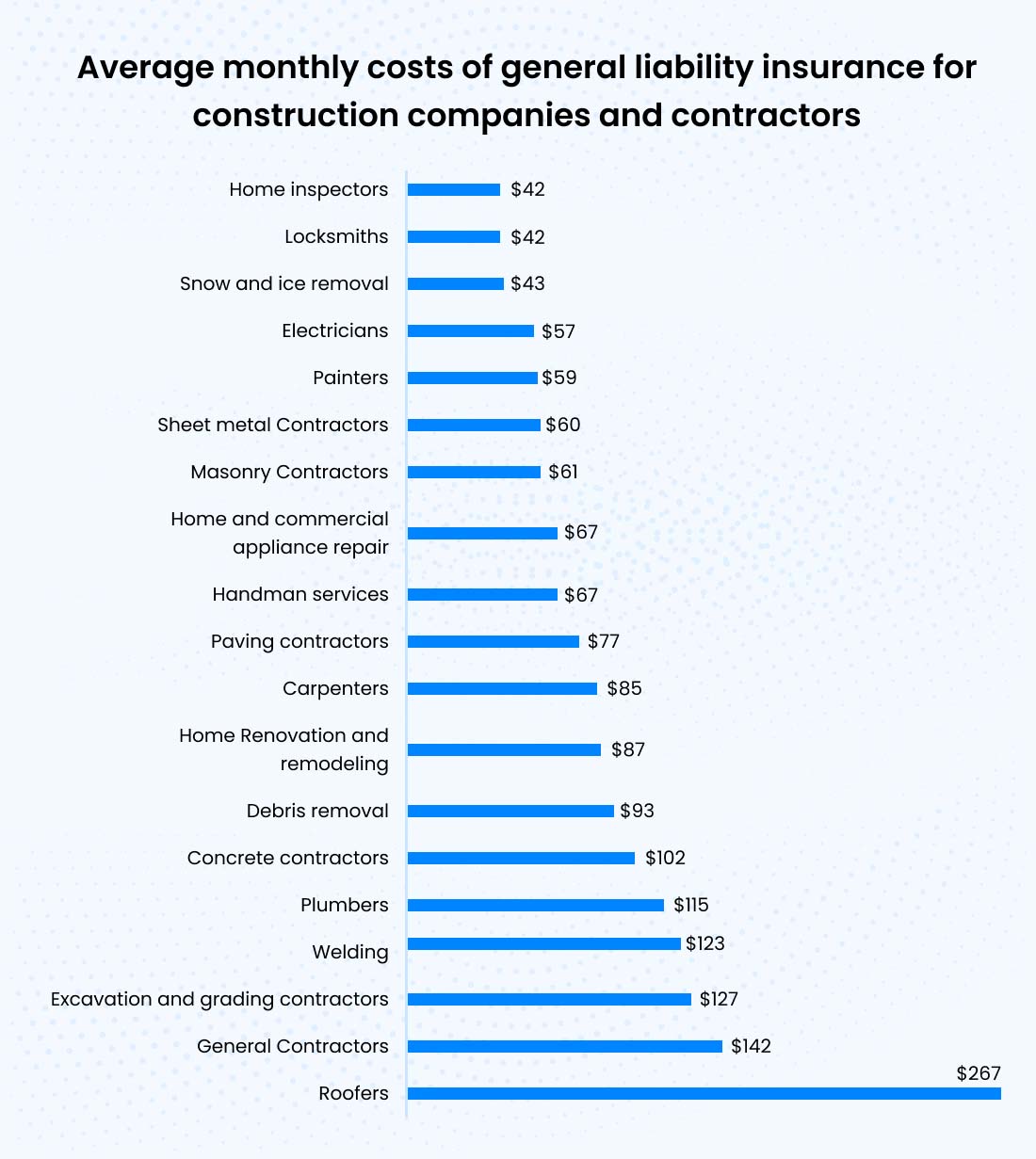

Here is a stat showing the average monthly cost of general liability insurance for construction companies and contractors.

Contractor Liability Insurance

Contractor liability insurance, also known as general liability insurance for contractors, is a type of insurance that helps protect contractors from legal claims arising out of their work.

What’s there in liability insurance for a general contractor? The coverage provided by contractor liability insurance typically includes:

Bodily Injury and Business Property Damage Coverage

This covers any damages caused to third parties due to your negligence or the negligence of your employees at the job site. For example, if you accidentally cause water damage to a client’s home while installing pipes, this coverage would help pay for repairs.

Medical Payments Coverage

Medical costs for non-employee injured parties at job sites are covered under this insurance category. Several elements impact premium rates such as business nature, geography, turnover, along with preferred policy extensiveness.

Prices fluctuate starting from $500 annually for fundamental plans up to over $10,000 regarding comprehensive packages. Exploring different carriers and reviewing propositions from multiple sources constitute crucial steps toward finding suitable arrangements fitting your requirements and fiscal constraints.

Obtaining contractor liability insurance ranks as an integral component securing your establishment against expensive litigation. Protection enveloping physical harm, asset destruction, private injury, and advertisement damages imparts tranquility, guaranteeing safeguards irrespective of unforeseeable circumstances.

General Contractors Insurance

General contractors insurance is a business insurance that covers general contractors and construction companies. This type of insurance can cover various risks associated with construction work, including property damage, bodily injury, and workers’ compensation.

What’s in the liability insurance for general contractors? Here is what contractors insurance covers; you can say general contractor insurance requirements:

General Liability: Protecting your business from legal claims associated with physical harm to individuals or damages to assets due to incidents occurring at a workplace is possible by acquiring this insurance coverage.

Workers’ Compensation: Injured workers may get compensation for medical bills and lost income via workers’ compensation.

Commercial Auto: If your business uses vehicles for transportation or deliveries, you will likely need commercial auto insurance to protect those assets.

Professional Liability: Coverage against legal action resulting from faults or omissions in your work; often called “Errors and Omissions” insurance.

Builders Risk: This coverage can protect buildings and materials under construction from fire, theft, vandalism, and other covered events.

However, the average annual premium for general liability insurance alone ranges from $742 to $3,698 for a contracting company, according to Insureon data cited by Forbes magazine. Other types of coverage may carry additional costs, so it’s important to talk to an agent about all your options before deciding.

Electrical Contractors Insurance

Electrical contractors insurance policy is specialized business insurance designed to protect electricians and electrical contracting firms from the unique risks they face while working on residential, commercial, or industrial projects.

What’s in the liability insurance for general contractors? Some common components of electrical contractors’ insurance include:

-

Professional Liability: Also known as Errors and Omissions (E&O) coverage, this protection safeguards electrical contractors against claims alleging negligent acts, errors, or omissions committed during the performance of their professional services.

General Liability: The general liability insurance contractors provide broad coverage for unexpected incidents that might arise during day-to-day operations, such as slips and falls on the job site, property damage caused by faulty installations, and bodily injuries to non-employees.

Workers’ Compensation: General Liability Insurance for Contractors Most states require employers to carry workers’ compensation insurance, which pays for injured employees’ medical expenses, lost income, and disability. This insurance may shield businesses from claims made by injured workers.

Commercial Auto: This general liability insurance contractor, designed explicitly for business-owned vehicles utilized during daily operations, Commercial Auto insurance affords protection comparable to standard automobile policies but tailored towards organizational usage instead of private drivers.

Tools and Equipment: Protecting valuable machinery, handheld devices, diagnostic instruments, and other necessary gear employed regularly in an electrician’s line of duty, Tools and Equipment coverage safeguards against unforeseen damages, theft, or losses.

Business Owner’s Policy (BOP): Consolidating several vital elements into one streamlined package, Business Owners Policies combined General Liability, Property insurance, and occasionally other relevant protections like Crime or Data Breach coverage within a single agreement.

Annual premiums may extend across wide margins ranging between $500 and $25,000 or beyond, subject to precise variables impacting each situation.

Who Needs Contractors Insurance?

While we discuss how you can have cheap contractor insurance or what is liability insurance for general contractors, anyone who works as a contractor, whether they are self-employed or run a small business, should consider getting contractor insurance.

This includes general contractors, electricians, plumbers, carpenters, roofers, painters, landscapers, HVAC technicians, and many others. Proper insurance coverage can protect contractors from significant financial losses related to property damage, bodily injury, and other issues that may arise during work.

Brian’s Contracting Business & Similar 1200+ Contractors Multiples Leads and Revenue by 300% in 2026.

Use Moon Invoice, A Modern Contractor Software that is specially tailored to manage & grow contractors’ businesses.

Contractor Insurance Requirements

General contractor insurance requirements can vary based on factors such as the specific trade, size of the business, and local regulatory guidelines. That said, here are some common aspects considered when determining contractor insurance needs:

-

Type of Services Offered: Different trades present varying degrees of inherent risks necessitating particular forms of coverage. For instance, electricians deal primarily with electrical systems posing shock hazards. In contrast, roofers tackle heightened elevations, amplifying fall dangers – both demand targeted safeguards addressing respective perils.

Business Structure: Whether operating solo as an independent contractor versus managing a team influences insurance obligations. Employers usually bear added responsibilities like Workers’ Compensation coverage to insulate against employee-related casualties.

Size of Projects: Undertaking larger or more intricate assignments warrants extra precautions given the magnified complexity and corresponding probability of mishaps. Big ventures commonly mandate higher liability limits plus specialized riders addressing exclusive challenges tied to elaborate tasks.

Value of Equipment: Contractors reliant heavily on expensive machinery, apparatus, and tools necessitate ample protection against possible damages, theft, or loss. Special provisions exist catering specifically to equipment preservation extending beyond generic policies.

5 Ways to Save on Contractors Insurance

Finding affordable business insurance or cheap contractor insurance involves taking several steps to ensure you get the best possible coverage at the lowest cost.

1. Obtain Comparative Quotes

Acquire estimates from multiple insurers offering similar plans to identify competitive pricing points among available alternatives. By comparing rates, you increase your chances of discovering favorable deals suiting budget constraints without compromising the required levels of protection.

2. Optimize Bundled Packages

Consider consolidating essential coverages under single umbrella policies, called Business Owners Policy (BOP).

These packages typically integrate crucial elements such as general liability, property damage, business income interruption, and sometimes even crime or cybersecurity protection modules – all wrapped together within a single agreement framework.

3. Establish Robust Safety Programs

Demonstrate commitment towards maintaining safe operational environments by implementing documented safety programs.

Properly executed measures to minimize accident risks can translate into tangible cost savings via potential premium reductions offered by appreciative insurers recognizing your proactive efforts.

4. Leverage Trade Association Affiliations

Joining reputable trade or industry bodies featuring sizable member networks may enable access to negotiated group rates on workers’ compensation insurance.

Participating insurers willing to extend these advantages usually seek organizations boasting diverse yet compatible member businesses sharing comparable operational risks. Investigate possibilities associated with affiliations and explore resulting discount prospects.

5. Adjust Commercial Vehicle Insurance Deductibles

Assess commercial car insurance arrangements and deliberately raise deductibles, which refer to out-of-pocket contributions payable before insurers step in to cover remaining claim amounts.

Higher deductibles equate to decreased insurer liabilities, translating into correspondingly reduced premiums.

Weigh carefully, though, since increased personal financial accountability accompanies this decision; select levels manageable amidst sudden incident occurrences.

How to Become a Construction Estimator

How Does Contractors Liability Insurance Protect Your Business?

Contractor liability insurance serves as a protective shield for your business, safeguarding you against unexpected events that might lead to financial hardships. This type of insurance helps cover costs when you face accusations of causing injuries or property damage at job sites or claims that your work mistakes resulted in financial losses for others.

Construction insurance packages include a combination of two critical forms of liability coverage:

General liability acts as the foundation of robust insurance protection for contractors. Since many contractors frequently operate on properties owned by others, the possibility of incidents such as scratched flooring due to a ladder or trip hazards posed by extension cords cannot be ignored. General liability insurance offers coverage against such instances, helping safeguard your assets and reputation.

Errors and omissions insurance, or professional liability insurance, covers circumstances where clients allege that you failed to deliver promised services adequately. Even if these accusations prove unfounded, defending your business against them can be costly.

How Much Does Contractors Insurance Cost?

Determining the cost of contractors insurance involves considering various factors, including:

Number of Employees

Workers compensation insurance costs rise proportionately with the number of employees in your organization.

Prior Claims History

Your previous business claims history holds substantial weight in calculating insurance costs. Insurers thoroughly assess this aspect to determine charges.

Insurance Coverage Needs

The selection of coverage types and policy limits significantly impacts insurance costs. Choosing higher coverage amounts generally leads to increased premiums.

Additional Pricing Factors

Other contributing elements in estimating costs encompass business assets, owned property, location, and the magnitude of your payroll. Each component contributes uniquely to shaping overall insurance expenses.

The Most Used Contractor Software For 2026. Trusted by 8500+ Contractors Like You.

Use Moon Invoice, A Modern Contractor Software that is specially tailored to manage & grow contractors’ businesses.

Conclusion

Accidents, injuries, and property damages are bound to happen while working in the construction industry or having a contracting company. Hence, selecting an appropriate contractor insurance is a wise move.

Besides this, if you are a contractor looking for an invoicing solution then Moon Invoice can do the job for you. It is for all-size businesses, you can use it if you are a freelancer too! It empowers you to create professional invoices in a few simple steps.

FAQs

What is The Cheapest Construction Insurance?

Why is Contractor Insurance Important?

What is General Contractor Insurance?

What Type Of Insurance Do I Need For The 1099?

What Is Contractor Liability Insurance Coverage?

Jayanti Katariya is the founder & CEO of Moon Invoice, with over a decade of experience in developing SaaS products and the fintech industry. He holds a degree in engineering. Since 2011, Jayanti's expertise has helped thousands of businesses, from small startups to large enterprises, streamline invoicing, estimation, and accounting operations. His vision is to deliver top-tier financial solutions globally, ensuring efficient financial management for all business owners.