Late Payment Fees Definition

Late payment fees are the charges that businesses often impose on their clients when payments are not made within the specified deadline.

Chasing your clients and urging them to settle outstanding payments is a common scenario for many businesses. However, this late payment can negatively impact your business’s cash flow. That is why business professionals opt to charge late payment fees to prevent late payments.

Of course, charging the late payment on the invoice is an ideal solution to this problem. But will it be worth it without proper knowledge of it?

What is a late payment fee? What amount do businesses need to charge as late payment fees? What are the applicable terms and conditions, and how do you make your client aware of them? If you are seeking the genuine answers to these questions, then it will be worth reading this article.

Our words will represent the story of late payment fees, so read them carefully while enjoying your favorite coffee!

📌 Key Takeaways

- Late payment fees are applicable when the client’s payment is pending even after the due date.

- Businesses can enhance their timely payment by applying late payment fees.

- Flat rate and percentage forms are two methods of charging a late payment fee.

- A standard interest rate for late payment invoices is 1% to 2%.

- Professionals should always clearly state the overdue payment fee terms and conditions on invoices, quotes, and contracts.

Do You Know?

In the USA🗽, the average credit card late fee is $30.50, with a maximum fee of $41.

What Is a Late Payment Fee on an Invoice?

Late fees on invoices are additional charges that businesses impose when clients fail to make payment by the due date. The major purpose of late fees is to encourage clients to make on-time payments.

Late invoice payment covers a flat fee or a percentage charge. Additionally, business professionals should always be aware of local laws when charging late fees. Understanding the impact of late payment is important, as late payment charges depend on state law and the type of business. Generally, businesses allow their customers to pay invoices within 7 to 14 days.

Is Charging Late Fees Legal?

Yes, charging late fees is legal; however, a company should mention the terms and conditions in the invoice. Companies should always provide details about late fees before starting the project or selling a product. This prevents any misunderstandings or issues that could negatively impact the overall business billing.

🔎Track all Your Pending Invoices Digitally with Moon Invoice

Experience the real-time tracking of invoice status and act accordingly. Quickly get insight into outstanding payments. 💵

What Is a Grace Period?

A grace period is the amount of time during which a client can make a payment without incurring late payment fees after the payment deadline has passed. This time is given by the business owners/vendors.

There are no late payment fees applicable during the grace period. Business professionals should clearly define the grace period within their contracts. A typical grace period is 3 to 10 days. This grace period is vital in maintaining a positive client relationship.

What Key Points to Consider When Charging Late Payment Fees?

After understanding the late payment fee meaning, let’s focus on the key points to consider when you charge the missed payment penalty:

- An original invoice must clearly state the due date and late payment fees.

- Mention the payment terms in an invoice regarding the late payment fee.

- Make your client well aware of the late payment policies.

- Consider local law when applying for late payment fees.

- The late fees should be nominal, in line with market standards.

- You must provide a grace period to build goodwill in the business-client relationship.

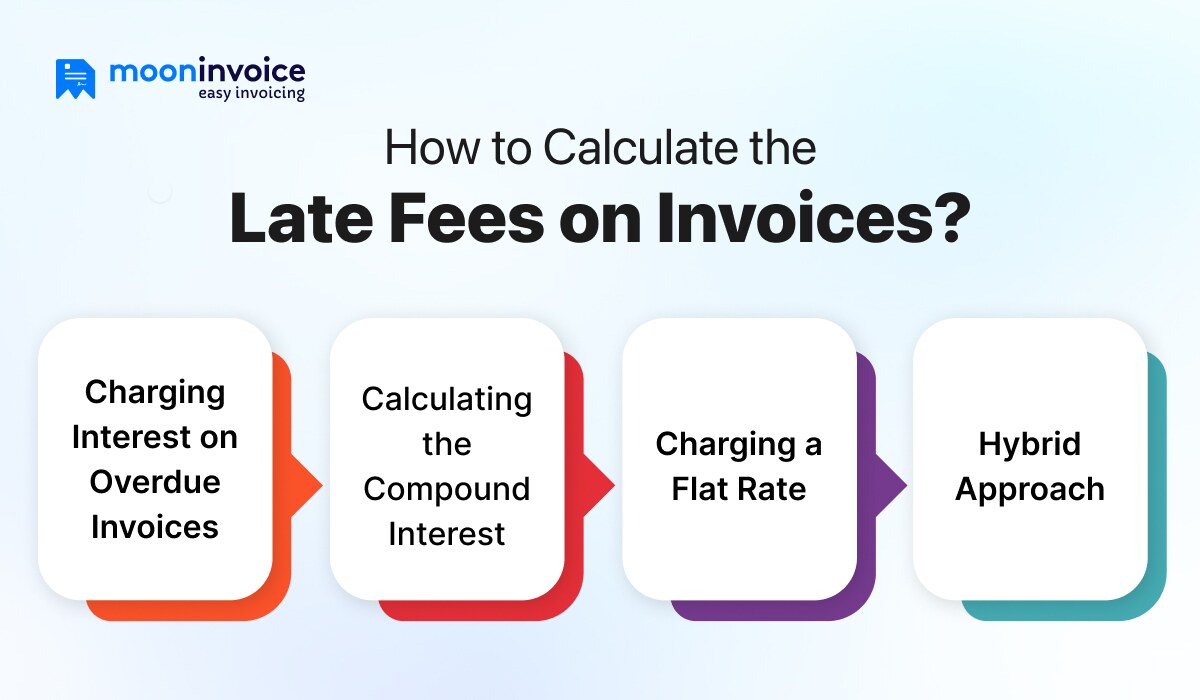

How Do You Calculate the Late Fees on Invoices?

Businesses can charge late fees, which may be in the form of late payment interest or a flat rate. Let’s understand the condition with an example of a late payment fee.

1. Charging Interest on Overdue Invoices

Calculating interest charge is straightforward using the following formula:

Assume a due invoice with an amount of $10,000 and an interest rate of 1%. The interest charge will be as follows:

$10,000 x 1% = $100

So, total late amount charge will be = $10,000 + $100 = $10,100

2. Calculating the Compound Interest

Compound interest is calculated based on the total due amount along with the previously applied interest charges.

Let’s understand this with an example: a due invoice of $1,000 at a 10% annual interest rate is applicable for a Net 30 days.

For a 10% yearly interest rate, the monthly interest rate will be 0.83%. (10% annual interest rate/12 months)

$1000 x 0.0083 = $8.33

$1000 + $8.33 = $1008.33

This is the amount that will be due after 30 days of payment.

Now, if the invoice remains unpaid for the next 60 days, interest will be calculated on the new amount, which was calculated for 30 days.

$1008.33 x 0.0083% = $8.369

$1008.33 + $8.36 = $1016.69

Now, this will be the due amount after 60 days of nonpayment.

Therefore, a new interest fee will be calculated based on the revised amount from the previous month.

3. Charging a Flat Rate

In a flat-rate charging approach, the customer is charged a fixed late fee, which can be paid on a weekly or monthly basis, depending on the amount. Various factors like industry standards, local laws, and business type define the fixed amount.

4. Hybrid Approach

Combining the flat fee with an interest rate leads to hybrid late fees. For instance, if the initial past-due fee (late payment charge) is $10 on every invoice, the interest rate will be 2% for every 30 days of nonpayment thereafter.

Late Payment Fees Don’t Work – What to Do?

There are several options to consider when late payment fees are not working. Some of them are as follows:

Get Flexible

If your customer is having difficulty making full payment, you can offer flexibility by providing an installment payment option to your client. This will make it easy for your client to make the payment and also help your business reduce late payments.

Sending Reminder

Your client accidentally missed a payment. A gentle reminder from your end is usually enough to prompt a client to make a payment. This is a common approach when business professionals send payment reminders to the client.

Contacting a Debt Collector

Companies can hire a debt collector, which is also known as a collection agency. These agencies chase customers on behalf of businesses after 60 days. Business professionals need to give some charges to these debt collectors, either in a percentage form or a flat fee.

Taking Legal Action

When every effort fails, a business has a legal weapon to use. This helps businesses to recover the due payment easily with the help of a lawyer. However, professionals should always choose this option when no other way is left.

State-Wise Maximum Invoice Late Fees in the USA

Here is the complete tabular form of applicable maximum invoice late fees and grace periods in different states of America.

| State | Maximum Late Fee | Grace Period |

|---|---|---|

| Alabama | No | 7 days |

| Alaska | No | 7 days |

| Arizona | No | 5 days |

| Arkansas | No | No |

| California | No | No |

| Colorado | No | No |

| Connecticut | No | 9 days |

| Delaware | 5% per month | 5 days |

| Florida | 5% of the past due amount | 15 days |

| Georgia | No | No |

| Hawaii | 8% per month | No |

| Idaho | 5% | 10 days |

| Illinois | $20 or 20% maximum | No |

| Indiana | No | No |

| Lowa | $60 per month when the balance is below $700, and a maximum of $100 per month when the balance is more than $700. | No |

| Kansas | No | No |

| Kentucky | No | No |

| Louisiana | No | No |

| Maine | 4% per month | 15 days |

| Maryland | 5% per month | 15 days |

| Massachusetts | No | 30 days |

| Michigan | No | No |

| Minnesota | 8% per month | No |

| Mississippi | No | No |

| Missouri | No | No |

| Montana | No | No |

| Nebraska | No | No |

| Nevada | 5% per month | No |

| New Hampshire | 5% per month | No |

| New Jersey | No | No |

| New Mexico | 10% per month | No |

| New York | $50 or 5 percent per month | 5 days |

| North Carolina | $15 or 15 percent per month | No |

| North Dakota | No | No |

| Ohio | No | No |

| Oklahoma | No | No |

| Oregon | 5% per month | No |

| Pennsylvania | No | No |

| Rhode Island | No | No |

| South Carolina | No | No |

| South Dakota | No | No |

| Tennessee | $30 or 10% per month, whichever is greater | 5 days |

| Texas | No | 5 days |

| Utah | No | No |

| Vermont | No | No |

| Virginia | No | 5 days |

| Washington | No | No |

| Washington, D.C. | 5% per month | 5 days |

| West Virginia | No | No |

| Wisconsin | $20 or 20% paper per month | 5 days |

| Wyoming | No | No |

What Are the Alternatives to Charging Interest and Late Fees?

Don’t like Maths & calculations? No worries! Several alternative options are available to help you recover your past-due invoices. Here are those:

Ask for Upfront Payment

This is a common approach that businesses follow for unpaid invoices. Requesting advance payments can secure your finances and business. You can request full payment or partial payment as needed.

Establish a Customer Communication

Establishing direct and clear communication with your client helps you prevent late payments. Ask them about the issues they are facing regarding payment. Additionally, inform them that late payments may lead to high late payment charges.

Selling Outstanding Invoices

Companies can adopt an invoice factoring process and sell their outstanding invoices to a factoring firm. The company then offers an immediate revenue stream. This option is suitable when your client is unable to make the payment, and you can’t wait for a long time.

Offering Payment Incentives

You can opt for an invoicing factor, where the lender purchases the outstanding accounts and, in return, gives your business funds. This is a common approach to improving business cash flow.

Provide Payment Plans

This is the best approach when your client faces financial difficulties. You can offer some payment flexibility and let the client pay the amount in installments. This will be mutually beneficial for both parties, as the client will be able to pay the amount easily, and your business will not suffer from financial difficulties.

What Are the Ways to Avoid Unpaid Invoices?

What is a late payment fee? After unlocking the answer, let’s understand how to avoid unpaid invoices. These overdue bills ruin the company’s financial health. Therefore, professionals should treat them carefully. The following strategies work better to avoid unpaid invoices:

Offer Multiple Payment Options

Offer multiple payment options and allow your clients to make payments at their convenience. This approach works better to reduce due invoices. This prevents the generation of unpaid invoices while streamlining the billing process.

Automate Invoicing

Free invoicing software, such as Moon Invoice, offers automation to save professionals time. Additionally, it also improves accuracy. This automation streamlines the billing process and helps prevent unpaid invoices.

Rewarding Discounts

Discounts always attract clients. Use them to attract clients’ attention to your billing and provide a markdown for their prompt payment. For example, if the customer makes the due payment within 7 days, then offer a 2% to 3% discount.

Also Read:free vs paid invoicing software

Tracking Unpaid Invoicing

Monitor all unpaid invoices and determine the number of outstanding invoices. Once you have determined this, please take the necessary action to convert them into paid invoices. Professionals can ease this process by adopting automation.

What Is the Strategy to Create a Late Fee Policy?

A business must have a clear and fair late payment fee policy, as it prevents confusion and enhances clarity regarding late fees for overdue payments. Additionally, businesses must know the right strategy for creating this policy, which is described below:

Define Your Charging Model

A business can charge a flat rate, interest, or a combination of both. Therefore, before outlining the late fee policy, a proper justification should be provided for selecting the appropriate model.

Decide the Amount

Different businesses charge different amounts for late payment fees, depending on the nature and size of the business.

When Is the Policy Applicable

You must be clear about when the policy comes into effect. What will be the criteria for charging a late fee for payment due? Should I allow a grace period to the client or charge late payment fees immediately after the due date passes? You must have a clear understanding of these questions.

Frequency of Sending Reminders

Set the frequency of sending reminders for outstanding balances. They may be sent daily or only after a delay of three or more days. You must choose the frequency that helps you reduce your late payments.

Do You Want to Eliminate Late Payments?

We are here for you! Automate your payment reminders and enhance the payment process with Moon Invoice.

Go for the Best Payment Setup for Your Business

Are you still following the manual process in your business? It can be a big enemy that could ruin your game. On the other hand, reputable invoicing software like Moon Invoice can be a valuable tool for invoicing.

The software offers peer-to-peer invoicing solutions to streamline your invoicing process. Business professionals can create professional invoices quickly and easily without compromising accuracy. Additionally, it is also simple to send invoices to clients through WhatsApp & email.

However, choosing the right payment setup is another challenge for professionals. With the various payment platforms available, it’s not easy to finalize the best-suited one, but you can get it!

Utilizing Moon Invoice can enhance your billing process and elevate your business to the next level through automated payment reminders, clear due dates, recurring invoice functionality, and seamless online payment integrations. Professionals can also track invoices in real-time and customize their payment terms and conditions. They can clearly define the late payment policy.

Wrapping Up

Professionals’ aim is not to loot clients through late payment charges. Instead, they are the right solutions to overcome late payment issues in the business. Additionally, business professionals should possess the necessary knowledge to manage late payment fees effectively. This is necessary to keep the business’s billing and financial flow active and on the right track.

Also, you must choose the right billing software as your partner to ensure consistent billing processes. Power your business with Moon Invoice!

Frequently Asked Questions

What Is a Typical Late Payment Fee?

What Is the Late Payment Penalty?

How to Calculate Late Rent Fees?

What Is the New Late Fee Law?

What Is an Ideal Late Fee Percentage?

Is a Late Payment Fee Legal?

Jayanti Katariya is the founder & CEO of Moon Invoice, with over a decade of experience in developing SaaS products and the fintech industry. He holds a degree in engineering. Since 2011, Jayanti's expertise has helped thousands of businesses, from small startups to large enterprises, streamline invoicing, estimation, and accounting operations. His vision is to deliver top-tier financial solutions globally, ensuring efficient financial management for all business owners.