TL;DR

A term gross means whole or total; therefore, gross income refers to the total income you earn as wages, compensation, or other sources of income. With keen awareness, you can simplify your tax filings and overall financial management. Determining gross income from a W-2 involves considering the amount in Box 1 and adding all applicable deductions.

Whether it’s about filing taxes or applying for a loan, understanding gross income is essential. For US citizens, the W-2 form plays a critical role in summarizing your annual earnings.

This document provides the required details of earnings. Unfortunately, many people have no idea of how to use this document to track income. As a result, they struggle when filing taxes for the first time, applying for a loan, and planning their finances.

Let’s check out how to calculate gross income from a W-2 here.

📌 Key Takeaways

- Understanding gross income is important for tax filing and financial planning.

- Gross income is always different from take-home income because of deductions.

- The gross income on the W-2 form is never shown directly. However, to calculate it, you need to consider Box 1, which reflects taxable wages.

- Accurate calculation of gross income helps to prevent financial misreporting and tax errors.

- Bonus and overtime pay are mentioned in the gross compensation on the W-2.

About 50% of Americans have no idea how to fill out their tax forms, and nearly 64% find tax filing stressful.

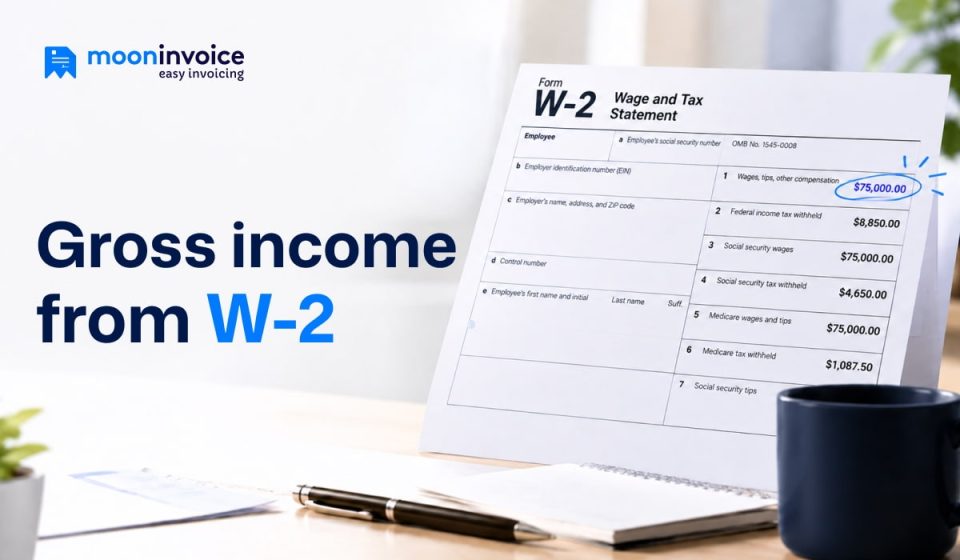

What is a W-2 form?

A W-2 form is a U.S. tax document that an employer gives to its employees, showing the taxable income, wages, and other compensation earned by employees in the year. The document is shared at the end of January every year.

As an employee, you use this document to report your earnings to the IRS and to file your return during tax season. The key structure of the W-2 form is as follows:

Wages Earned

- Box 1 (Wages, tips, and other compensation) – This represents the taxable income after deducting pre-tax deductions.

- Box 3 (Social Security wages) – This box represents the earnings subject to Social Security tax. The amount is different from Box 1.

- Box 5 (Medicare wages and tips) – This box shows income subject to Medicare taxes, which differ from other wage amounts.

Taxes Withhold

It shows the amount of tax that was deducted from your total paycheck throughout the year.

- Box 2 (Federal income tax withheld) – The total amount of Federal taxes the employer withheld.

- Box 4 (Social Security tax withheld) – The total amount of taxes that the employer withheld as Social Security tax.

- Box 6 (Medicare tax withheld) – The total amount of taxes the employer withheld as Medicare tax.

- Box 17 (State income tax withheld) – The total amount of state income tax deducted from the total salary, if applicable.

- Box 19 (Local income tax withheld) – Any local or city income taxes that are deducted from the paycheck.

Employee benefits and deductions

The W-2 form also includes employee benefits and deductions, which are as follows:

- Box 12 (Benefit and deduction codes) – This box includes deductions for 401(k), employer-sponsored health insurance, and other retirement plans, each with a specific letter code. Some of the codes are as follows:

-

→Code D: 401(k) retirement contributions

→Code E: 403(b) retirement contributions

→Code W: Health Savings Account (HSA) contributions

- Box 13 (Retirement plan checkbox) – It indicates your participation in the employer-sponsored retirement plan. Other than that, you can also mention the third-party sick pay that you receive from a third party instead of your employer.

- Box 14 (Additional information) – You can mention union dues, tuition assistance, charitable contributions, and other deductions here.

What is the difference between W-2 vs W-9 form?

What is gross income?

Gross income refers to the total income an employee earns before any deductions are applied. This total income is not limited to the salary received from the employer. It includes property, money, and the value of received services.

Gross earnings may include wages, bonuses, freelance earnings ($400 or more), rental income, and other sources.

For instance, suppose a person earns income in the following ways –

- Wage – $3,60,000 annually.

- Bonus earning – $1000

- Freelancing income – $200

At the end of the financial year, when he calculates gross income, he needs to consider all of the above earnings, regardless of their sources.

$3,60,000 + $1000 + $200 = $3,61,200

So, the gross income of the person is $3,61,200

Why is it important to understand gross income?

Understanding gross income helps you determine your taxable income and the net income you actually receive.

Calculating the total taxable income

It becomes easier to identify the total taxable income once you understand the gross income. You can determine your adjusted gross income (AGI), which is useful in determining various deductions.

You can also determine your modified adjusted gross income (MAGI), which is important for the tax process. It includes certain added-back deductions in addition to AGI, so it usually equals or exceeds AGI.

Determining the net income

With a clear understanding of gross income, it is easy to determine the total take-home pay. This take-home pay is the amount of money you receive after taxes and other deductions.

For full-time employees in the US, the employer already deducts the applicable tax based on the W-4 form. The applicable taxes are State Income Tax, Social Security Tax, Insurance, and Medicare.

Streamline the loan process

Lenders often use gross income to evaluate your financial condition. Gross income gives clear insights and helps to make informed decisions when processing the loan. Thus, understanding annual gross income on a W-2 is an important metric when you apply for a loan.

Finding the credit limits

Credit card issuers often use gross income to determine the credit limits. A higher income clearly indicates the financial stability of an individual or a business. Thus, it becomes easier for lenders to assess repayment capacity when determining the credit limit.

How to determine annual gross income from a W-2?

Determining the gross income from a W-2 is not a big deal. However, a systematic approach is required. So, how do you calculate gross income? Here are the steps:

1. Start with Box 1

Understanding gross income on a W-2 form requires recognizing that Box 1 (wages, tips, other compensation) does not contain certain pre-tax benefits. This amount will be lower than your total gross income because of certain deductions applied. Always treat Box 1 as a starting point when you think about how to find gross income on a W-2.

2. Add pre-tax deductions

To estimate the true gross income, you need to add back the following deductions:

- Health insurance premium

- Retirement contributions such as 401(k)

- Other pre-tax benefits

3. Sum all the additional sources of income

You must include other sources of income and add them all together. These sources can be any of the following

- Rental income

- Interest earning

- Taxable alimony

- Capital gains

- Dividends

- Gigs or freelancing work

4. Add all the income sources together

Finally, you need to sum the income reported on the W-2 form and from other sources.

Knowing how to find gross pay on your W-2 is useful for understanding your taxable income and overall financial planning & management

On the W-2 form, Box 3 and Box 5 show Social Security wages and Medicare wages & tips, respectively. If these boxes have a higher value than Box 1, it means pre-tax deductions are in effect.

What is gross monthly income?

Gross monthly income refers to the total amount of money that you earn in a month before any kind of deductions. These deductions may be taxes, insurance, retirement contributions, and other withholdings.

Unlike annual income, which is calculated yearly, gross monthly income is calculated on the basis of each month.

How to calculate gross monthly income?

Similar to annual income, gross monthly income can be calculated. However, in this case, you need to divide your annual income by 12 to get the monthly figure. Here are the steps you need to follow when thinking about how to find gross income on a W-2, month-wise.

1. Find your annual income

When using the W-2 form, look at Box 1 (wages, tips, and other compensation).

2. Add pre-tax deductions

This is optional, but it gives a more accurate figure. To get more accurate information, you need to add back pre-tax deductions. Additionally, you can add insurance, retirement contributions, and other benefits.

3. Divide by 12 to get the monthly gross income

Convert the total annual income to monthly income by dividing it by 12. The end result is the monthly gross income that you get each month before any deductions.

What is adjusted gross income?

Adjusted Gross Income (AGI) is the total income that an individual earns after certain specific deductions. The following are some deductions that are allowed by the IRS:

- Student loan interest

- Retirement contributions

- Educator expenditure

- Health savings account (HSA) contributions

- Self-employment deductions

The simpler formula for calculating the adjusted gross income is as follows:

One of the major benefits of tracking AGI is that you get the right idea of reducing your eligible deductions legally. This helps to reduce your tax burden and save your money. It also contributes to correct tax filing and financial planning.

Role of Moon Invoice in managing gross income

While analyzing your W-2 form and determining your gross income is straightforward, you further need effective financial management. Especially when you work as a freelancer, gig worker, or run your own small business as a side profession.

To streamline your tax reporting, you can manage your invoices, track and organize receipts, and maintain accurate records of every payment. Without this, determining your accurate gross income becomes difficult, which ultimately affects the taxation.

Using Moon Invoice, you can enhance your overall income management. The software lets you create professional digital invoices with ready-made templates. Get tax-inclusive invoicing, as the system supports multiple taxes and automatically calculates them at invoicing time. Hence, leaving no room for error.

Thus, you can simplify income tracking and maintain clean, organized records. You can also manage your expenditures efficiently. Categorize your expenditures for better understanding and financial control.

Overall, this invoicing software delivers a smart, efficient solution for faster, more accurate, and more organized financial management.

Still handling your finances manually?

Choose Moon Invoice – save time, reduce errors, and manage your finances with ease.

Final words

In the end, understanding how to calculate gross income from a W-2 form is essential. With a clear approach to calculations, you can streamline your tax filing and stay organized in your overall financial reporting and management. Instead of just knowing the figures, you must also understand the value of gross income and its impact on overall financial decisions.

FAQs

What is a gross income on a W-2?

What is the formula for gross income?

Can I calculate adjusted gross income from a W-2?

How can I calculate annual gross income?

Is W-2 Box 1 the same as gross income?

We at Moon Invoice, are the best minds behind smarter invoicing and seamless business growth. We love to solve financial problems and keep providing effective tips through our blogs, newsletters, and social media channels. As a team, we continue exchanging ideas about growing financial challenges and smart use of automation tools.

![How to Calculate Retained Earnings [Example + Formula]](https://mi-blogs.s3.amazonaws.com/mi-live/blog/wp-content/uploads/2023/12/29115729/HowtoCalculateRetainedEarning.jpeg)