You have secured a new beaming contract, but the advance payments aren’t rolling in yet. With this cash flow strain, staying focused on providing excellent work for your clients can be challenging.

Most contractors or agents cannot cover construction costs out of their wallets or personal loans, and borrowing money is also not an option because it may lead to a lien, which would obstruct the project’s development.

But don’t worry; you can do more with contractor financing for customers.

While you can undertake large projects, contract financing is your way to fulfill them and quickly fill the gaps in cash flow. Contractor financing companies can effectively fulfill contracts and grow your business if you qualify for a small-business loan.

Let us start with understanding what contract financing is!

What is Contractor Financing?

Contractor financing is a financial instrument or loan for advance funding. This option is commonly available to small contractor firms, and it pays for the supplies, labor, and other expenditures related to a contractor’s task.

It can assist company owners in managing the financial aspects of construction or maintenance projects. It includes credit lines, contractor loans, and other financial instruments tailored to the construction industry. This type of finance can be used to satisfy urgent demands and project deadlines.

Contractor finance allows organizations to undertake larger purchases at lower rates by lowering their debt-to-equity ratio and improving their balance sheet.

There are several types of financing:

- Business Credit Cards: Lower credit limit than credit lines for unsecured credit.

- Business Lines of Credit: It can be as required but has a fixed limit.

- Factoring: A company takes on your potential customer accounts for a fee and then gives you a percentage.

- Trade Credit: You can buy goods or services on agreed-upon payment terms.

- Equipment Financing: You can manage day-to-day expenses, earn rewards or cashback, and separate personal and business spending.

Boost Your Cash Flow: Deliver 30% Faster Payments!

Get paid quicker with our efficient invoicing tools. Access funds faster with Moon Invoice.

How Does Contractor Financing Work?

Instead of standard loan requirements factors like collateral, personal credit, or business profit, contractor finance concentrates its loan underwriting on the value of a contract obtained by the company.

Using finance from contractor financing companies is the best method to handle cash flow problems on your projects. It is an alternate flexible funding source where conventional financing is far more challenging. Additionally, it is paid once duties are finished.

A standard company loan and contract finance for contractors differ in crucial respects. To begin with, compared to a conventional secured loan, it is a riskier unsecured loan. As a result, the lender may exercise greater caution and examine more factors than usual before issuing a business loan.

The lender may check the conditions of the contract, including the price, timeframes, and payment milestones, before approving the transaction. Better funding alternatives and interest rates are available to businesses with solid credit ratings.

The payback terms are set up to correspond with the payment terms of the contract, and their applications are often restricted to contract-related costs. Typically, the loan finance for contractors ranges from 20% to 30% of the whole contract value. Depending on the type of loan and the terms, contractors may receive up to 90% of their money upfront.

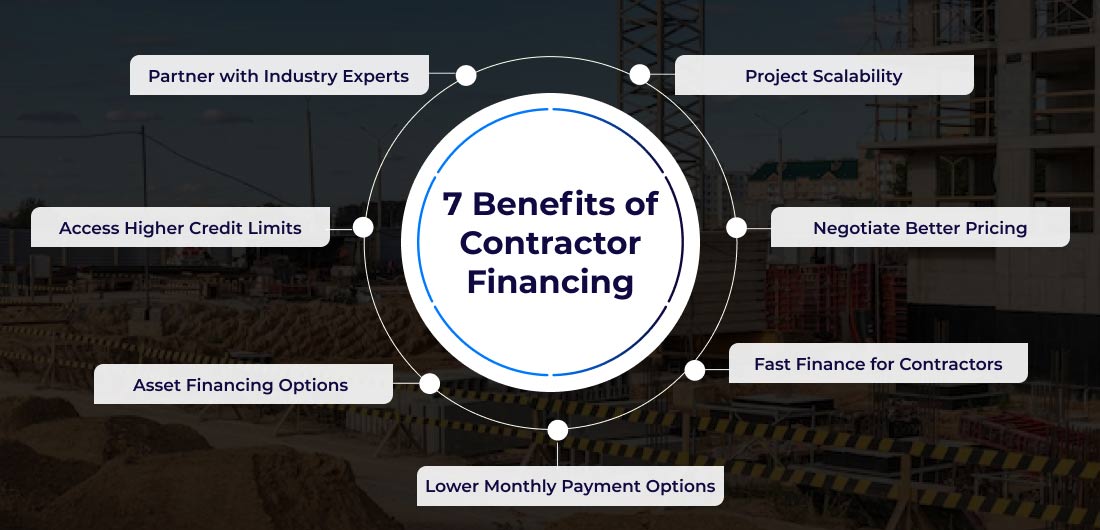

7 Benefits of Contractor Financing

Here are some of the top seven benefits of offering contractor financing for customers and businesses:

1. Partner with Industry Experts

You will get access to experts in the pertinent industry sectors who are knowledgeable about the operations of businesses much like yours. You can ask contractor marketing ideas to help grow your business, improve your financial situation, and increase sales.

2. Access Higher Credit Limits

Additional credit management support is available if you wish to delegate the task of collecting late accounts receivable to a team of professionals.

3. Asset Financing Options

Asset financing may also be advantageous when buying equipment. By doing this, the significant up-front expenditures of purchasing equipment are eliminated. These fees may be dispersed across more extended time frames to increase your company’s liquidity.

4. Lower Monthly Payment Options

The amount you owe to contractor financing companies may be paid in smaller monthly payments over a more extended period when you eventually receive funding for a project.

5. Fast Finance for Contractors

With project-based finance, the transaction frequently moves forward considerably more quickly since your financing partner is aware of your requirement for speed to maintain the timeliness of your building project.

6. Negotiate Better Pricing

With upfront cash for higher-quality materials or equipment, you can negotiate better pricing with potential customers. You can get better deals on your needed resources and free up cash.

7. Project Scalability

With cash in hand, you can win highly competitive construction bids with accurate construction project costing and scale your contracting business to larger projects. You can also offer customer financing with easy payment options and loan terms, making your business model sales process easy.

Invoice Faster: Moon Invoice Saves You 15+ Hours Monthly

Focus on growing your contractor business, not paperwork.

When to Use Contract Financing?

Knowing when to use contract financing is essential for contractors and customers alike. It involves understanding the circumstances and scenarios where financing options make the most sense.

Here is when to use contractor financing for your business:

- When you want to win bigger bids. Using contractor financing to start winning bigger contracts can be a good way to start growing.

- When you want to grow your business. Seeking larger contracts might help your organization develop in the long run, but it can also cause cash-flow gaps.

- When you do not have any finance requirements outside of your contract. As these loans are aligned with a specific project with a suitable contract, contractor financing it is best if you require funding in no other sector of your business.

- When you are unable to get a regular loan. If you require additional business finance, a typical term loan or a line of credit may be a better option.

- When you don’t have any substantial assets to utilize as collateral. Contractor loans do not require other assets to be collateralized because your contract serves as collateral.

- If you have a good relationship with your client. Financing options perform especially well if you have trust in the client with whom you are working. Offering financing to your customers makes sure that the payment options are clear.

Alternatives to Contractor Financing

Let’s assume you could not secure a financing option or did not find one that suits your needs. So, what do you do next?

Well, here are a few options.

1. Invoice Financing

Similar to a contractor loan, invoice finance or accounts receivable financing process protects your loan amount from receiving unpaid invoices. It might manage cash flow issues just like contract financing. This financing could be more advantageous for smaller contract-based firms. You can simplify billing and manage accounts receivable using invoicing and billing software like Moon Invoice. With a contractor invoice template, it makes requesting payments and keeping track of all of your payments and financial commitments simpler.

2. Small-Business Term Loans

While many people utilize contractor loan products when they can’t get traditional term loans for contractors, ensuring you qualify is crucial, especially if you need money for more than one contract. Term loans are less expensive in the long term and improve your company’s credit.

3. SBA Loans

SBA 504 and 7(a) loans may be an excellent choice if you need help being approved by regular lenders, especially if you’re a small business.

4. Business Lines of Credit

Business lines of credit, including corporate credit cards, may be an excellent substitute for short-term contractor loans since they are revolving and can be regularly utilized to plug cash-flow shortages on many contracts.

Join 10,000+ Satisfied Users: Get Moon Invoice

See why businesses have relied on us for over a decade. Discover the power of streamlined invoicing with Moon Invoice.

Conclusion

Small construction business owners need working capital to stay afloat, and during tight cash flow, securing contractor financing and contractor insurance can help.

To ensure you are eligible for the right kind of funding when required, contractors should also work with their accountants or financial managers to continuously improve their monitoring and reporting techniques.

Smaller contractors support their local communities with jobs, fair wages, and benefits. And with contractor financing, they can go for the win! For additional help with your cash flow, you can also choose the famous invoicing and accounting tool Moon Invoice. With its automation feature and contractor invoice template, you can grow your business exponentially.

FAQs

How to offer financing as a contractor?

Why should contractors consider offering financing?

Is there a risk associated with the contractor financing process for customers?

Jayanti Katariya is the founder & CEO of Moon Invoice, with over a decade of experience in developing SaaS products and the fintech industry. He holds a degree in engineering. Since 2011, Jayanti's expertise has helped thousands of businesses, from small startups to large enterprises, streamline invoicing, estimation, and accounting operations. His vision is to deliver top-tier financial solutions globally, ensuring efficient financial management for all business owners.